On the 19th local time, the Federal Deposit Insurance Corporation of the United States issued a statement saying that new york Community Bank had agreed to buy the signature bank that was closed on the 12th. The future of the larger Silicon Valley bank, which was taken over by the federal agency, is still uncertain. On the 19th, some media broke the news that the Federal Deposit Insurance Corporation (FDIC) was considering splitting up the assets of Silicon Valley Bank, which has not been officially confirmed.

The signatory bank was "accepted" by Silicon Valley Bank or "separated"

The Federal Deposit Insurance Corporation of the United States announced in a statement on the 19th that it had reached an agreement with Qixing Bank, a wholly-owned subsidiary of new york Community Bank, to sell most of the deposit business and part of the loan business of the signatory bank. Starting from 20th, all 40 branches of the signatory bank will be managed by Qixing Bank. The transaction does not include about $4 billion in deposits related to the digital banking business of the signatory bank. In addition, the loan business of about $60 billion of the signatory banks is still under the management of the Federal Deposit Insurance Corporation, which is still to be disposed of.

On the other hand, the US media quoted people familiar with the matter as saying on the 19th that the Federal Deposit Insurance Corporation is seeking to split and sell the closed Silicon Valley Bank. According to reports, Silicon Valley Bank is expected to be split into at least two parts for sale. Among them, the private banking business of Silicon Valley Bank will be sold separately, which mainly serves high-net-worth people, and the deadline for bidding is 22; Another part of Silicon Valley Bank — — That is, the "transitional bank" set up by the Federal Deposit Insurance Corporation to take over the deposits and assets of Silicon Valley banks will be sold as another part.

The US government’s "one guarantee to the end" or brewing greater risks

Bank of America "thundered" one after another, causing market concerns. The industry is worried that the spread of panic will trigger a run on other financial institutions in the United States. To this end, the US Treasury Department, the Federal Reserve and the Federal Deposit Insurance Corporation have previously announced actions to "cover the bottom" for depositors of the incident bank, including customers with deposits exceeding $250,000. Previously, according to the standard, the maximum insured amount of each bank depositor with deposit insurance was $250,000. The practice of American regulators to "guarantee the bank deposits to the end" caused public concern.

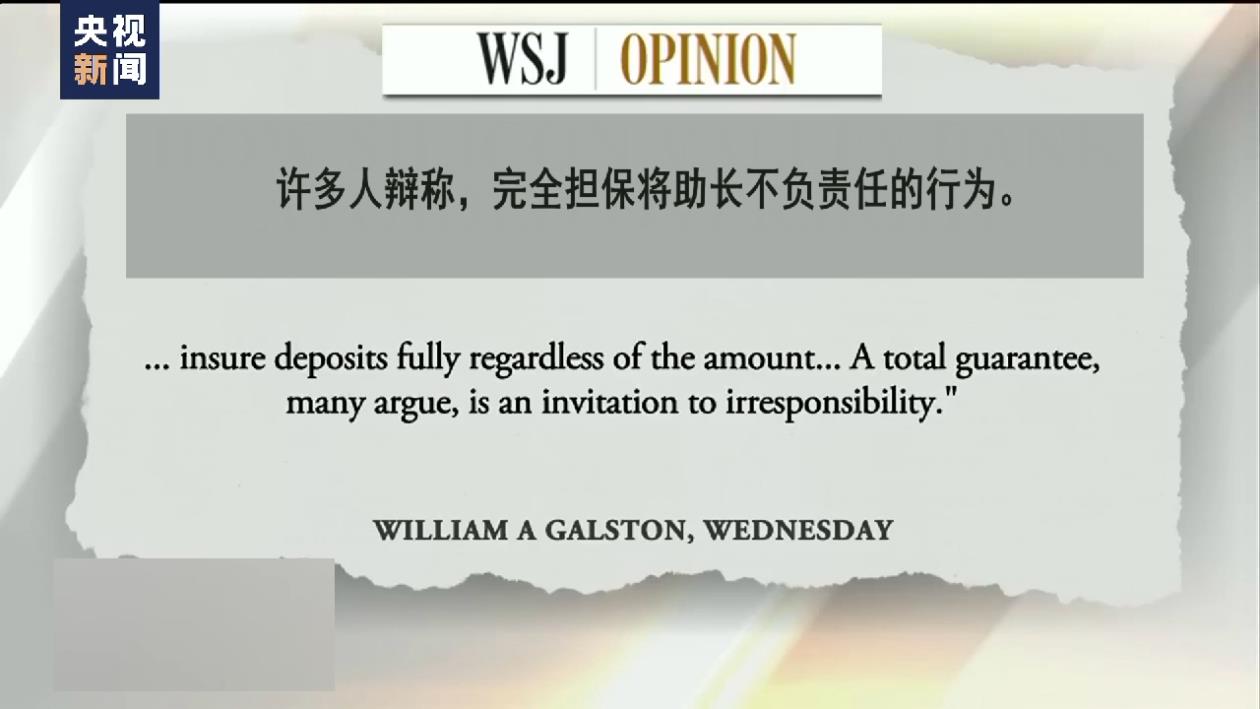

"The Wall Street Journal" recently wrote, "Many observers are worried that ignoring the $250,000 deposit insurance ceiling will lead to the call that no matter how big the amount is, it will be guaranteed to the end. Many people argue that full guarantees will encourage irresponsible behavior. " What The Wall Street Journal is actually talking about is the so-called "moral hazard" problem, that is, when the actors don’t have to take full responsibility for their own actions, they are more inclined to take greater risks, which may cause the financial markets in the United States and even the world to fall into turmoil.

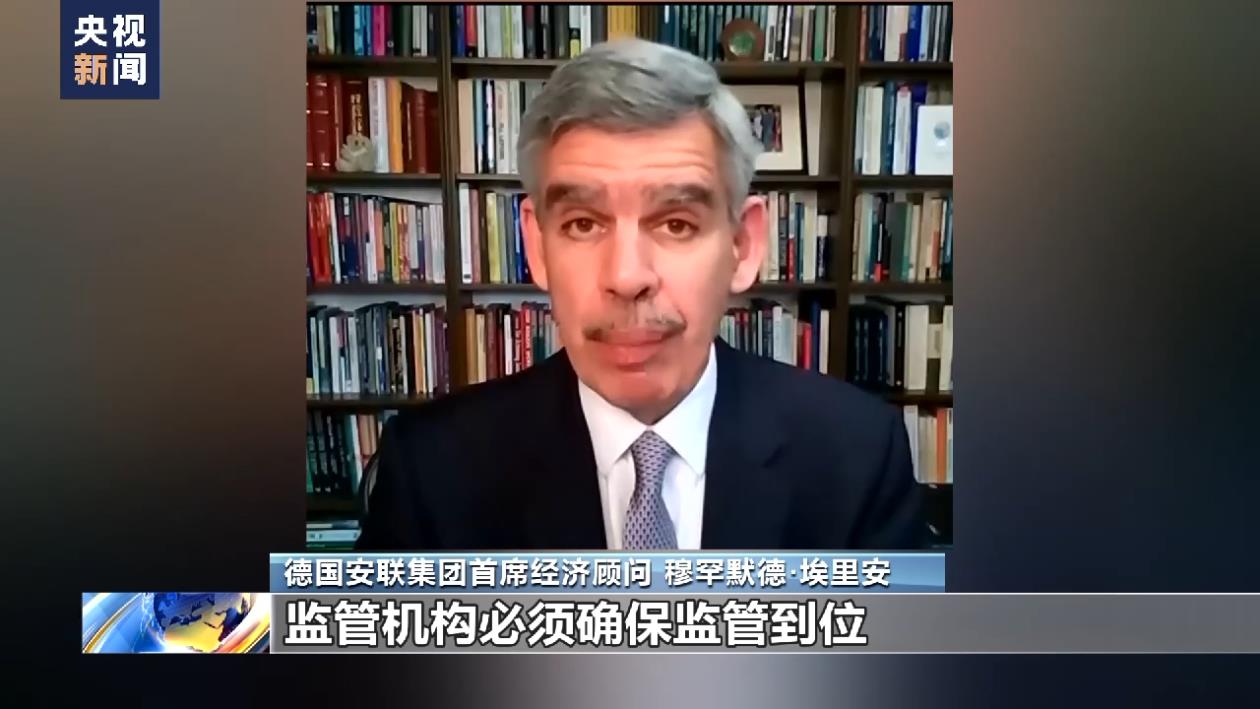

Mohamed El-Erian, Chief Economic Advisor of Allianz Group: Will this lead to irresponsible behavior? Obviously, there is this risk, which is why we should control the "moral hazard" and the regulators must ensure that the supervision is in place.

Steve Sosnik, Chief Strategy Officer, Intone Securities Group, USA: This is the real problem. American politicians take all the responsibility for the banking crisis in the United States. Once business and politics are mixed together, things will change. I hope that the upper limit of deposit insurance will be raised. As you said, it seems reasonable to mention 1 million dollars. However, if there is no deposit insurance ceiling at all, it will indeed lead to "moral hazard".

The wool is on the sheep, and the funds will be passed on to taxpayers.

Although the US government has repeatedly claimed that the relevant "bottom" will not use taxpayers’ money, according to US media analysis, this is not the case.

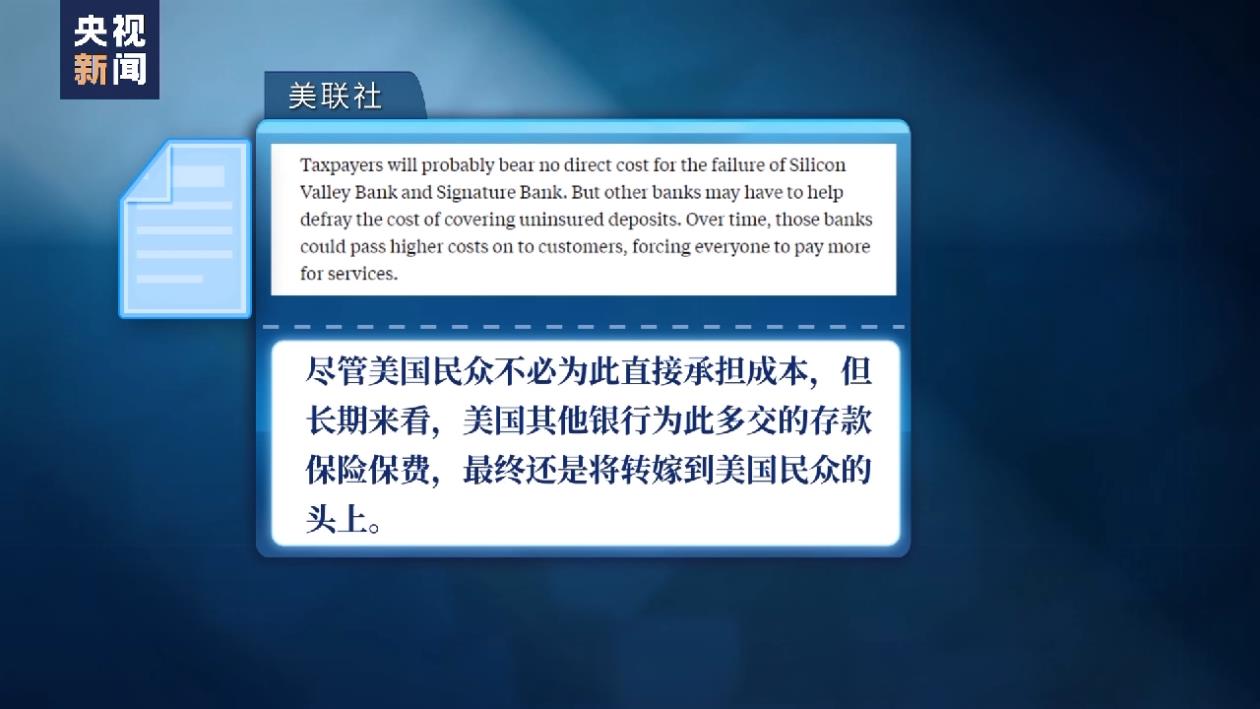

The Associated Press published an article on the 17th, entitled "Will Americans finally bear the costs for bank mistakes? According to the analysis of the article, the deposit insurance fund comes from the premium paid by the bank for deposit insurance. The purpose of its establishment is to provide depositors with funds within 250,000 US dollars when the bank is closed. But now, the Federal Reserve and other institutions say that all deposits in the incident bank will be paid in full — — This means that the Federal Deposit Insurance Corporation of the United States actually uses the funds of customers who have paid deposit insurance to cover the full amount of customers who have not paid deposit insurance.

The Associated Press said that although the American people do not have to bear the cost directly, in the long run, the deposit insurance premiums paid by other American banks for this purpose will eventually be passed on to the American people.

Steve Sosnik, Chief Strategist Officer, Yingtong Securities Group, USA: The question is how the deposit insurance ceiling will be reassessed and passed on to bank customers in the form of higher premiums. Because the insurance premium paid before is up to 250,000 US dollars (deposit), there is no upper limit.

US Senator: Bank of America and Railroad "chase short-term profits at the expense of everything else"

At the recent hearing of the US Senate Banking Committee, Ohio Senator Sherrod Brown compared the closure of the Silicon Valley Bank with the "poison train" derailment accident in Ohio in early February. He said that these two incidents reflected the common ground of American banking and railway industries: colluding with politicians and pursuing maximum profits at all costs.

Senator Sherrod Brown, Ohio, USA: I want to say a few words about the people in East Palestinian City, Ohio and the closure of the Silicon Valley Bank. These two things have one thing in common: the company follows the business model of Wall Street and pursues short-term profits at the expense of everything else. They have been helped and abetted by corporate lobbyists and politicians here (Congress), who have weakened the rules of this application to protect the people we serve according to their own wishes. Now, working-class people in Ohio and across the United States have paid the price.

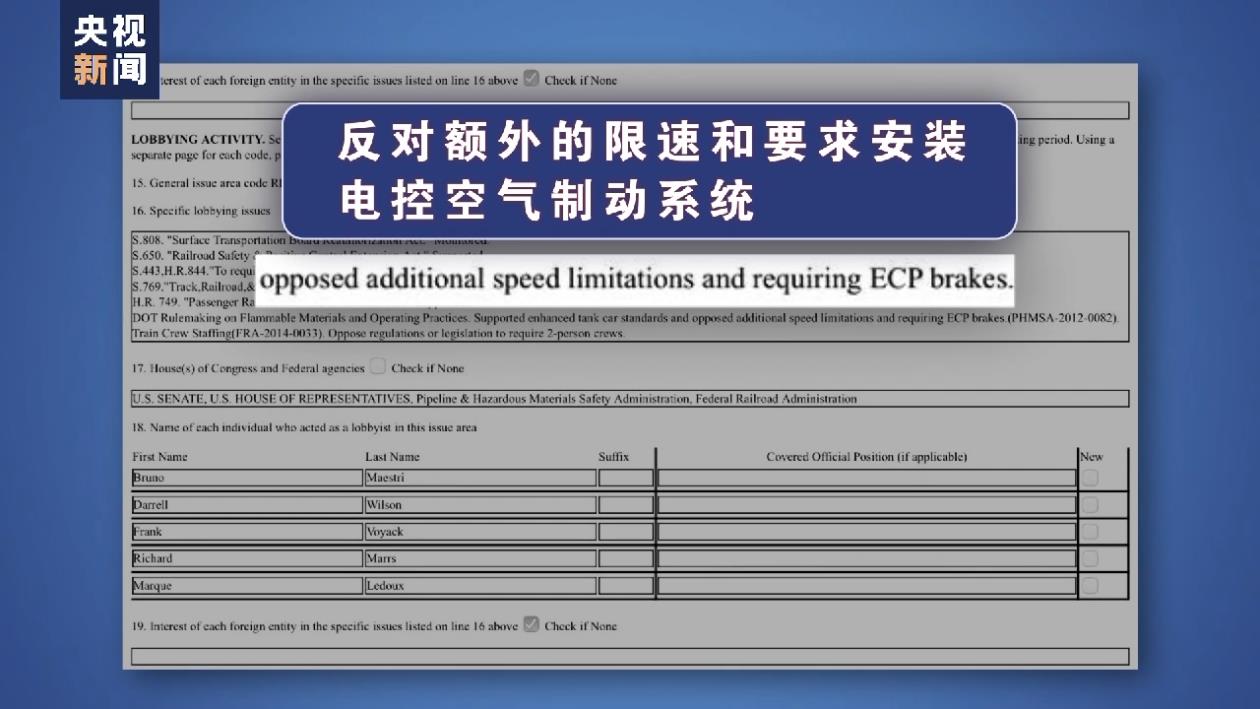

According to the lobbying documents of Norfolk Southern Railway Company, which belongs to the "poison train" derailed in Ohio in 2015, the company lobbied Congress and the administrative agency responsible for formulating the rules of the Ministry of Communications to "oppose the additional speed limit and require the installation of ECP (Electronic Control Air Brake System)".

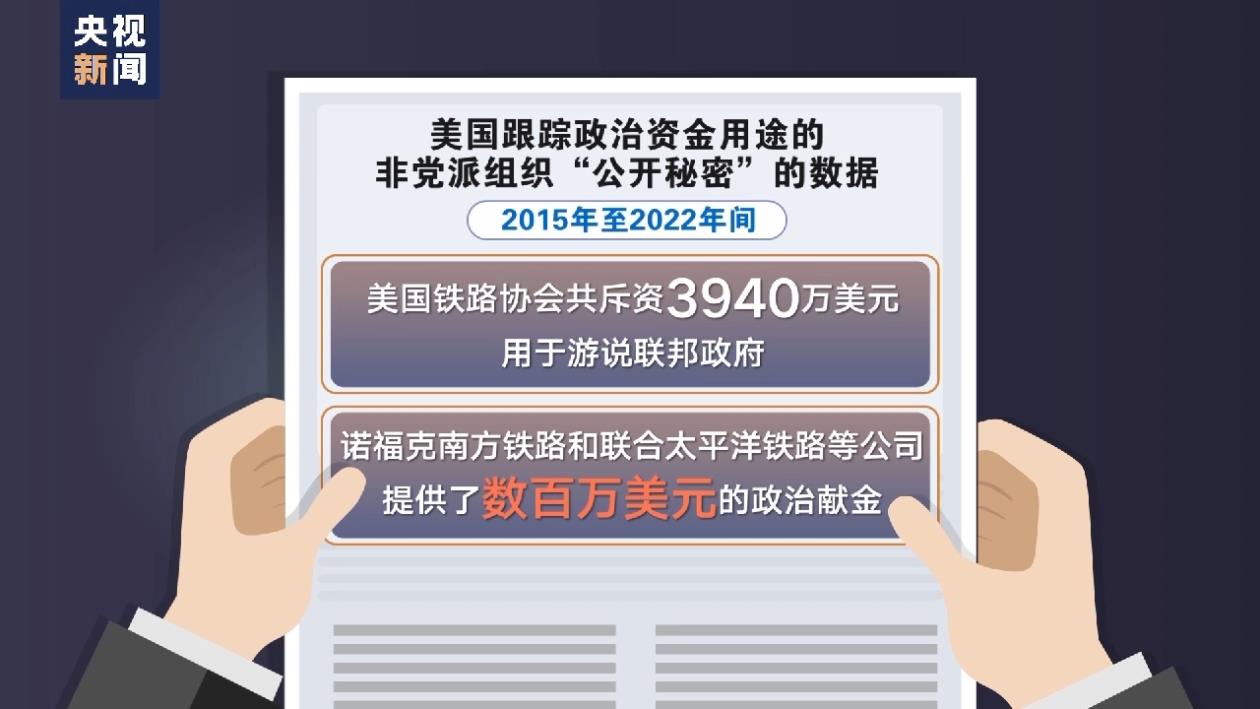

According to the data of "Open Secret", a non-partisan organization that tracks the use of political funds in the United States, from 2015 to 2022, the American Railway Association spent a total of 39.4 million US dollars to lobby the federal government. Among them, companies such as Norfolk Southern Railway and Union Pacific Railway provided millions of dollars in political contributions.

Senator Sherrod Brown, Ohio, USA: Think about the two most influential lobbyists in this country in the past 100 years, the bank and the railway. This is the cause of the 2008 financial crisis, which wiped out the savings of the working class and delayed a whole generation of young Americans. Wall Street certainly hasn’t changed its way of doing things. In the following years, the banks on Wall Street have been lobbying for the withdrawal of the safeguards we adopted after the crisis.

Senator Sherrod Brown, Ohio, USA: The now defunct Silicon Valley Bank spent hundreds of thousands of dollars to get rid of its CEO to attend the hearing. I guess he is unemployed now. He said that their banks should not be subject to strong supervision because "our activities and business model are low-risk". "Low risk", that’s what he said. We all know what they really pursue, profit maximization, whatever the risk.

In 2015, Baker, CEO of Silicon Valley Bank, personally lobbied the Senate to ask Congress to reduce the review of financial institutions and exempt a number of financial institutions, including Silicon Valley Bank. In 2018, the lobbying of Silicon Valley Bank finally succeeded. The US Congress raised the criteria for determining the existence of systemic risks in banks, and both Silicon Valley Bank and signatory banks were exempted from this supervision. According to the Daily Mail website, federal records show that from 2015 to 2018, Becker spent more than $500,000 on lobbying the federal government.